When Sam Altman was asked how a company with questionable profitability could justify $1.4 trillion in infrastructure commitments, he didn't blink. "If you want to sell your shares," he told the investor, "I'll find you a buyer." The exchange highlighted tensions around OpenAI's ambitious spending plans. One interpretation: in 2026, the market appears to increasingly reward not just AI companies that burn cash, but also those that translate intelligence into revenue at speed.

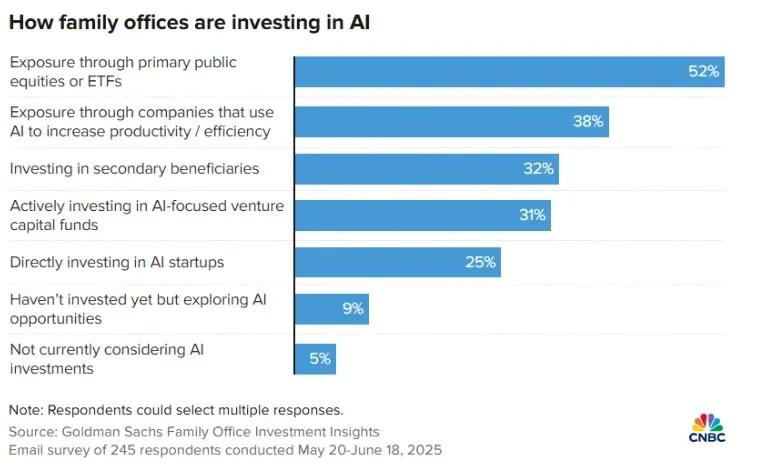

Many family offices appear to be rewriting their playbooks in response. 86% now invest in AI, with the technology ranking as a top conviction theme for the next five years, according to Goldman Sachs' 2025 Family Office Investment Insights report. But this capital may not be indiscriminate. While 52% access AI through public equities or ETFs, a smaller proportion invest directly in AI startups. The gatekeeping can be severe. The question for AI companies may not be whether family office capital exists, but rather how to architect revenue models that could capture it before competitors do.

The capital reallocation

The numbers suggest a story of patient capital potentially turning aggressive. Tech giants collectively invested aggressively in AI capital expenditures in 2025, with spending expected to keep climbing. Hyperscaler capex is forecast to exceed $600 billion in 2026, a 36% increase year-over-year. But family offices may not simply be following the hyperscalers. Many appear to be seeking out the companies that monetise this infrastructure without building it themselves.

Technology leads sector allocations, with 58% of family offices planning to overweight the area within the next year, and 51% already using AI in their investment decision-making. This data suggests strategic repositioning may be underway. As one BNY Wealth report notes, 83% rank artificial intelligence as a top conviction theme for the next five years. However, private market valuations may remain a barrier, with many family offices reportedly expressing concerns about growth-at-any-cost narratives overwhelming execution.

Revenue model 1: AI infrastructure: The "Picks and Shovels" play

Significant new data centre capacity is expected to be added between 2026 and 2030, potentially expanding global capacity substantially. As an example, OpenAI, Oracle, and SoftBank announced five new U.S. AI data centre sites under Stargate, bringing combined planned capacity to nearly 7 gigawatts and over $400 billion in planned investment over the next three years. Anthropic announced a $50 billion planned investment in American computing infrastructure, intended to build data centres with Fluidstack in Texas and New York.

The revenue model typically involves: long-term capacity leases with anchor tenants, colocation fees plus managed AI orchestration services, and inflation-protected escalating pricing. Data centre construction costs have increased significantly in recent years, with substantial capital requirements per megawatt.

Family offices may see appeal in 10-15 year asset lifetimes, tangible collateral, and returns tied to secular demand. Middle Eastern sovereign wealth funds are co-investing with BlackRock, Microsoft, and private equity in multi-billion-dollar partnerships. One potential attraction: recurring revenue visibility without betting on any single application layer. For more context on this sector, see our guide to investing in data centres.

Revenue model 2: Vertical AI SaaS: Niche dominance over horizontal breadth

SaaS valuations have seen substantial increases, with median primary valuations for seed rounds rising significantly year-over-year, according to industry analysts. Series A median primary valuations have similarly appreciated. But valuation may not be the whole story: retention often plays a critical role.

Vertical SaaS tends to exhibit lower churn because industry-specific solutions can become mission-critical, often report higher net revenue retention, and may command pricing power justified by domain expertise. The vertical SaaS market is estimated to be worth tens of billions of dollars as of 2025, with various industry reports projecting strong double-digit compound annual growth rates over the coming years.

Target sectors that appear to be gaining notable traction include: healthcare and life sciences (Benchling, a leading life sciences software platform, has achieved a valuation in the billions of dollars and reports strong annual recurring revenue growth), finance (risk management and regulatory reporting), logistics and freight (route optimisation and customs compliance), and real estate/hospitality, where AI is projected to add substantial value. Blue-collar workflows in manufacturing and field services have reported potentially strong unit economics, with some vertical SaaS companies reporting significantly lower sales and marketing spend compared to horizontal peers. For related insights, explore our analysis of AI-driven drug discovery.

Revenue Model 3: API-First and consumption models: Recurring revenue at infrastructure speed

Enterprise services were reportedly OpenAI's growth engine in 2025, with the company stating that a substantial number of businesses now pay for enterprise-grade AI products, and paid seats for ChatGPT workplace products reportedly growing significantly.

Anthropic has demonstrated similar momentum. At the beginning of 2025, less than two years after launch, Anthropic's run-rate revenue had grown to approximately $1 billion. By August 2025, just eight months later, run-rate revenue reached over $5 billion, potentially making Anthropic among the fastest-growing technology companies in recent years.

The revenue model typically combines usage-based metering (per-token API pricing), tiered API access (base access plus premium tiers for dedicated capacity and SLA guarantees), and hybrid subscription plus consumption models. Enterprise and startup API calls continue to drive revenue through pay-per-token pricing. Claude Code has reportedly taken off since its full launch in May 2025, already generating over $500 million in run-rate revenue with usage growing more than 10x in just three months, according to Anthropic.

Revenue mix and emerging monetisation models

OpenAI and Anthropic, for example, show distinctly different revenue compositions: Anthropic earns approximately80% of its revenue from enterprise customers, while the majority of OpenAI's revenue comes from consumers and increasing ChatGPT usage. Notably, only about 5% of ChatGPT's 800 million weekly users pay for subscriptions. To address this monetisation gap, OpenAI announced plans to test ads at the bottom of ChatGPT answers for free and "Go" tier users in the U.S. This emerging ad model represents an additional revenue stream beyond the B2B API and B2C subscription channels already discussed.

For those interested in understanding how private equity valuations work in technology companies, it's worth noting that API-first businesses may scale revenue without linear headcount growth and can exhibit software-like margins of 40-50%.

What family offices demand: Unit economics over narrative

Investment criteria often ranked by priority include:

- Recurring revenue visibility: ARR growth rates exceeding 50% with high net revenue retention

- Unit economics clarity: CAC payback under 12 months, LTV:CAC ratio above 3:1.

- Scalability without linear costs: Software margins above 60% gross or infrastructure with operating leverage.

- Defensive moats: Proprietary data, embedded workflows, regulatory compliance, ecosystem lock-in.

- Management quality: Proven track record scaling similar businesses, clear path to profitability.

AI startups tend to raise at higher valuations than their peers at the Series A stage, according to industry analysts. In public markets, the median AI market cap-to-revenue multiple has widely exceeded 10x, but these multiples are not uniform. The valuation premium appears to be selectively rewarding AI-native platforms, particularly those positioned as infrastructure or foundational layers, while potentially applying greater scrutiny to applied or derivative AI products. For investors evaluating opportunities across gaming and interactive entertainment or other emerging sectors, a similar pattern may hold: markets tend to reward execution, not just potential.

The capital appears to be there, but the gatekeeping can be severe

Substantial capital expenditure on data centres equipped to handle AI processing loads is expected to be required through 2030. The infrastructure is being built. The applications that justify it must demonstrate returns. Most family offices are investing in AI and leveraging it for data analysis, research, and portfolio optimisation. The fastest movers may be companies that combine predictable recurring revenue, proven unit economics, defensible positioning, and strategic validation.

The question may not be whether your AI company can attract family office capital. It could be whether your revenue model is architected to capture it before the window closes. As Acquinox Capital's investment approach demonstrates, later-stage pre-IPO opportunities across Next-Gen industries typically require institutional-grade revenue visibility and scalability. In an environment where intelligence is becoming increasingly accessible, the companies that monetise it with clarity and speed could play a significant role in shaping the decade ahead.

This article has been prepared using data and analysis from Goldman Sachs, BNY Wealth, Anthropic, Reuters, OpenAI and other sources as cited.

Published by Samuel Hieber