Waymo raised $16 billion at a $126 billion valuation in February 2026, reportedly the largest investment ever in an autonomous vehicle company. With 90% fewer injury claims than human drivers (Swiss Re data), 400,000+ weekly rides across six US cities, and a significant cost reduction in its 6th-generation hardware, Waymo is a deep technology company transitioning from proof-of-concept to commercial reality. Key risks include ongoing unprofitability, regulatory uncertainty, and competitive threats from Tesla and Chinese players.

The taxi driver doesn't exist. The steering wheel moves on its own. Another business commuter makes it on time to their meeting, without public transport, without a driver and it's reasonably affordable. This isn't science fiction. It's a Tuesday morning in San Francisco, and it's happening 400,000 times every week across America.

Waymo just raised $16 billion at a $126 billion valuation, more than doubling its worth in sixteen months. For institutional investors, this marks something rare: a driverless technology company transitioning from proof-of-concept to commercial reality, backed by quantified safety data and operational scale that few competitors currently match.

From Google moonshot to $126 billion juggernaut

Waymo's funding trajectory tells the story of autonomous vehicles moving from laboratory curiosity to investable infrastructure.

Funding timeline

Date | Round | Amount | Valuation | Lead Investors |

February 2, 2026 | Series D | $16.00B | $126.00B post-money | Dragoneer Investment Group, DST Global, Sequoia Capital |

October 25, 2024 | Series C | $5.60B | $45.00B post-money | Alphabet |

June 16, 2021 | Series B | $2.50B | Not disclosed | Silver Lake, CPP Investments, Mubadala Capital |

May 12, 2020 | Series A | $3.00B | $30.00B post-money | Silver Lake, CPP Investments, Mubadala Capital |

Source: PitchBook, a Morningstar company

Summary statistics

Metric | Value |

Total Capital Raised | $27.10B |

Current Post-Money Valuation | $126.00B |

Total VC Rounds | 4 (Series A–D) |

Financing Status | Venture Capital-Backed |

Business Status | Generating Revenue |

Headquarters | Mountain View, CA |

Source: PitchBook, a Morningstar company

The February round was led by Dragoneer Investment Group, DST Global, and Sequoia Capital, with Alphabet maintaining majority ownership.

Why the 180% valuation jump? In 2025 alone, Waymo tripled annual ride volume to 15 million trips, surpassing 20 million lifetime rides. The company now provides more than 400,000 paid rides weekly across six U.S. metropolitan areas.

As DST Global co-founder Saurabh Gupta stated, Waymo is "saving lives already, with significantly fewer serious injury crashes compared to human drivers."

Technology moat: Multi-sensor intelligence at significantly reduced cost

Waymo's 6th-generation autonomous system, launched in February 2026, represents a fundamental shift in robotaxi economics.

6th-generation hardware comparison

Specification | 5th Generation | 6th Generation | Change |

Cameras | 29 | 13 | -55% |

Lidar sensors | 5 | 4 | -20% |

Radar units | 6 | 6 | 0% |

Total sensors | 40 | 23 | -42% |

Cost | n/a | “Significantly reduced” | Significant cost reduction |

Source: Waymo, Automotive World

This contrasts notably with Tesla's camera-only approach. Waymo maintains that safety-critical autonomous systems require sensor redundancy beyond cameras only. The company's lidar provides 3D environmental mapping up to 500 metres in all weather conditions, something cameras cannot match in dust storms, heavy rain, or dense fog.

The 6th-generation system is the "product of seven years of safety-proven service amassed from driving nearly 200 million fully autonomous miles," Waymo states, providing operational learning no competitor can replicate.

The 90% safety advantage

Waymo's most defensible competitive moat is quantified safety performance.

A December 2024 study conducted with Swiss Re, one of the world's leading reinsurers, analysed 25.3 million autonomous miles across Phoenix, San Francisco, Los Angeles, and Austin.

Swiss Re Safety Study Results

Metric | Waymo vs Human Drivers | Waymo vs ADAS-Equipped Vehicles |

Property damage claims reduction | 88% | 86% |

Bodily injury claims reduction | 92% | 90% |

In concrete terms, across 25.3 million miles, Waymo recorded nine property damage claims and two bodily injury claims. Human drivers would typically generate 78 property damage claims and 26 bodily injury claims over the same distance.

This safety record directly impacts unit economics through reduced insurance premiums, accelerated regulatory approvals, enhanced consumer trust, and limited liability exposure.

Partnerships de-risking scale

Waymo's manufacturing and distribution partnerships address the primary obstacles to robotaxi scaling.

Manufacturing: Waymo operates a facility in Metro Phoenix with partner Magna International, targeting a capacity of "tens of thousands of units per year." The facility integrates 6th-generation systems onto multiple vehicle platforms with flexible production lines.

OEM partnerships: Hyundai is reportedly in discussions to supply up to 50,000 Ioniq 5 units, which would represent the largest single vehicle order in autonomous driving history. Geely's Zeekr provides RT minivans for current deployment. The Toyota partnership (announced April 2025) explores incorporating Waymo technology into personally owned vehicles, opening potential high-margin licensing revenue.

Ride-hailing integrations: Waymo vehicles operate through the Uber app in Austin and Atlanta, with Lyft integration in Nashville. These partnerships provide customer acquisition without marketing spend, tapping into platforms with hundreds of millions of users.

International expansion: London and Tokyo are confirmed as first international markets, targeting 2026 service start. These markets validate Waymo's technology across different regulatory frameworks, road configurations, and driving cultures.

Market position: Clear U.S. leader, global ambitions

Waymo operates a 24/7 fully autonomous ride service at commercial scale in the United States. Current footprint includes San Francisco, Los Angeles, Phoenix, Austin, Atlanta, and Miami, with expansion planned to additional US cities in 2026.

Competitive Landscape

Company | Status | Weekly Rides | Notes |

Waymo | Commercial | 400,000+ | US market leader |

Baidu Apollo | Commercial | 250,000-3000,000+ | China market leader |

Tesla | Supervised testing | Limited | Austin/Bay Area; safety supervisors on board |

Zoox (Amazon) | Testing | n/a | Targeting 2026 paid rides |

Cruise (GM) | Discontinued | n/a |

In San Francisco, Waymo has reportedly surpassed Lyft and commanded more than 20% market share within its operating domain.

Business model: path to profitability

Waymo operates a per-ride revenue model with pricing based on distance, time, and demand. At 400,000 weekly rides, Financial Times reports annual recurring revenue exceeds $350 million.

Secondary revenue opportunities include technology licensing (Toyota partnership signals OEM interest in software licensing) and data services for urban planning, insurance modelling, and automotive R&D.

Investment risks and realities

Regulatory uncertainty remains. Waymo issued software recalls in December 2025 after Texas officials reported robotaxis illegally passed school buses. In January 2026, a Waymo struck a child in Santa Monica (minor injuries reported), triggering new NHTSA scrutiny. However, Waymo's overall safety record provides regulatory tailwind.

Capital intensity persists. At current volumes, Waymo remains unprofitable with significant annual operating costs. The $16 billion funding round provides substantial runway, but scaling to profitability requires significantly higher ride volumes.

Competitive threats loom. Tesla aims to expand its robotaxi operations and leverage its manufacturing scale. If Tesla's vision-only approach proves viable at scale, its manufacturing capacity could overwhelm Waymo's OEM partnerships. China's Baidu Apollo benefits from state support and lower operating costs, though Waymo has no China presence.

Technology commoditisation risk exists. UK-based Wayve raised $1.5 billion in February 2026 for an "asset-light" licensing model, selling autonomous software to OEMs rather than operating fleets. If OEMs prefer in-house or licensed solutions, Waymo's vertically integrated model could face margin pressure.

The Investment Thesis

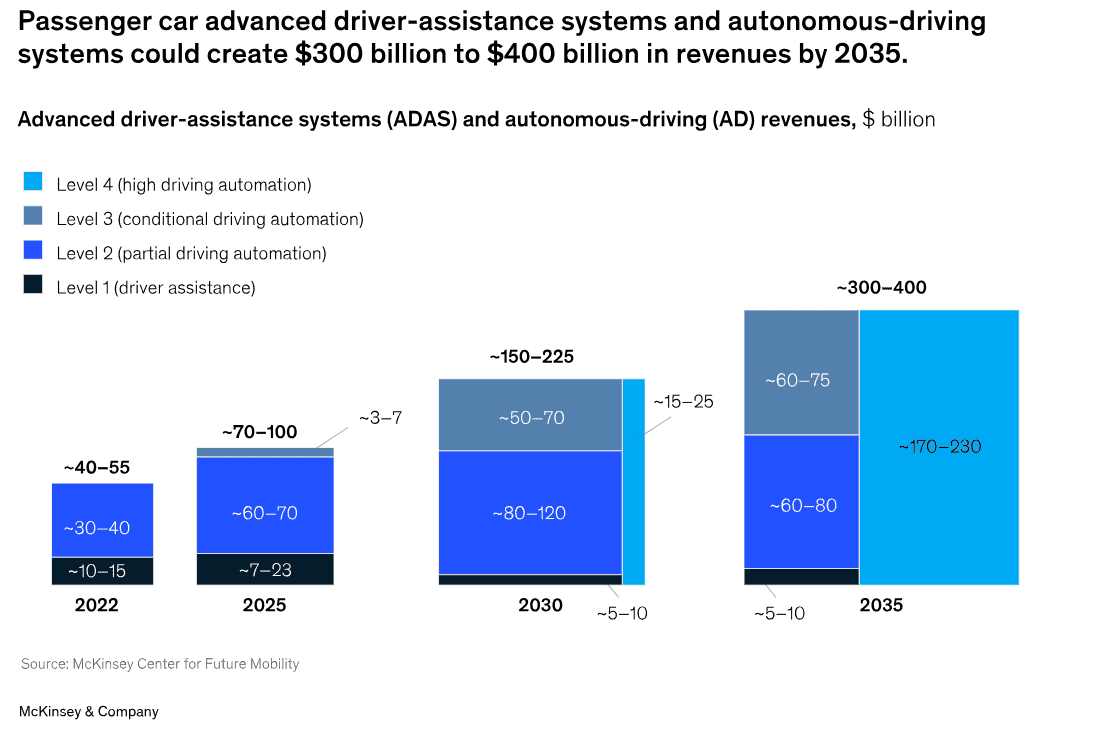

At $126 billion, Waymo trades at a significant premium to current revenue, a valuation that prices in dominant market share of an autonomous mobility market projected to reach $300-400 billion by 2035, according to McKinsey.

Waymo's valuation reflects five key premium factors: a technology moat built over 15 years and nearly 200 million miles; 90% claims reduction creating regulatory and consumer advantages; operational lead as the only commercial-scale autonomous service in the U.S.; multiple revenue opportunities for licensing, delivery, and international expansion; and Alphabet's deep pockets and technical expertise.

The bull case rests on proven safety superiority, operational scale demonstrating commercial viability, technology lead difficult to replicate, partnerships de-risking distribution and manufacturing, international expansion opening new markets, 6th-generation hardware reducing costs by 50%+, and patient capital from Alphabet.

The bear case highlights valuation requiring flawless execution, ongoing losses with profitability years away, competition from Tesla's manufacturing scale, regulatory risk from safety incidents, unproven profitability requiring significantly higher vehicle utilisation, market size uncertainty around personal ownership versus robotaxis, and geographic constraints to select urban markets.

From moonshot to transportation infrastructure

The daily commuter avoiding traffic stress. The visually impaired rider gaining independent mobility. These aren't edge cases, they're Waymo's 400,000 weekly customers.

For investors evaluating pre-IPO opportunities in autonomous mobility, Waymo represents a unique inflection point. The company has transitioned from science experiment to commercial operation, backed by institutional capital, quantified safety data, and expanding global presence.

The question isn't whether autonomous vehicles will transform transportation. It's whether Waymo's operational lead, safety moat, and partnership ecosystem justify pricing that assumes global dominance. For those with appropriate risk tolerance and extended time horizons, Waymo offers exposure to what may be the most significant transformation in mobility since the automobile itself.

Learn more about Acquinox Capital's approach to Next-Gen Industries and our latest insights on emerging technologies.

Published by Samuel Hieber