Four hundred billion dollars. That's roughly what Amazon, Microsoft, Google, and Meta will spend on AI infrastructure in 2026 alone. To put that in perspective, it's more than the GDP of Finland, and it's being deployed faster than any infrastructure buildout in modern history. If you're wondering where the real action in AI investing lies, forget the chatbots for a moment. The story is in the steel, silicon, and power grids that make intelligence itself possible.

Welcome to the data infrastructure gold rush, where sovereign wealth funds are behaving like venture capitalists, where a specialised cloud provider, Coreweave, trades at a ~$50 billion valuation, and where access to electricity matters more than access to talent.

The numbers tell the story

Apart from staggering capex spending numbers, these aggregate numbers don't capture the velocity. What we’re seeing isn't gradual expansion. It's a strategic race where falling behind means irrelevance. Across the four largest hyperscalers and Oracle, combined capex is widely projected to approach $600 billion in 2026, with nearly 75% expected to go towards AI infrastructure, the aforementioned $400 billion.

And then there's OpenAI's Stargate project, announced in January 2025 with a staggering $500 billion commitment over four years to build AI data centres across the United States. It's physical infrastructure being deployed at unprecedented speed.

Why Sovereign Wealth Funds are All In

For the first time in technology history, nation-states are leading the charge. Sovereign wealth funds deployed $66 billion into AI and digital infrastructure in 2025, with Middle Eastern funds dominating. Abu Dhabi's Mubadala invested $12.9 billion, Kuwait's sovereign fund committed $6 billion, and Qatar deployed $4 billion.

This isn't passive portfolio allocation. It's an industrial strategy dressed up as venture capital. Saudi Arabia's Public Investment Fund is building AI factories and semiconductor partnerships. UAE's MGX, for example, is part of Stargate alongside OpenAI and SoftBank, securing a strategic seat at the table where the future of compute is being designed. These governments view AI infrastructure the way previous generations viewed oil refineries or ports: as critical national assets that shape geopolitical power for decades.

Much like how OpenAI and Anthropic are becoming embedded in government systems, sovereign funds are securing long-term access to foundational AI capabilities through direct ownership of the infrastructure layer.

The economics: Scarcity drives pricing power

Unlike previous tech bubbles, where oversupply eventually crashed prices, AI infrastructure faces hard physical constraints that create genuine scarcity:

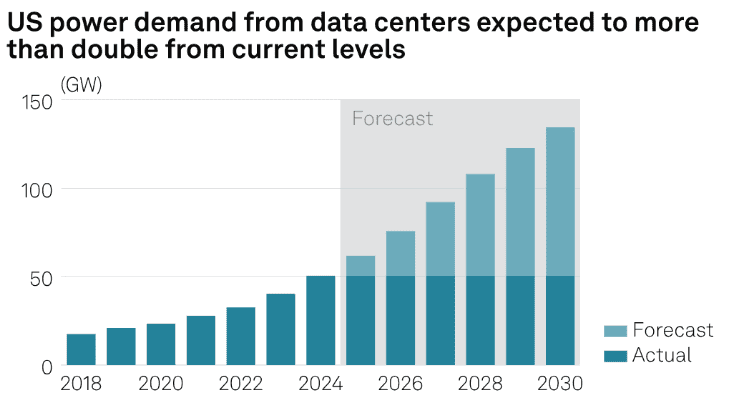

Power is the defining bottleneck. Data centres in the US will require 22% more grid power by the end of 2025 than a year earlier, according to S&P Global. By 2030, they'll need nearly triple today's capacity. Yet grid interconnection timelines stretch multiple years in major markets. Many companies are securing nuclear plant partnerships and building on-site generation just to keep projects moving.

GPU scarcity remains acute. High-bandwidth memory shortages mean delivery timelines for next-generation chips stretch months to years. NVIDIA's order backlog is measured in quarters, not weeks.

AI-optimised facilities command premium pricing. Traditional data centres require significant capital investment per megawatt to build, while AI-optimised facilities can cost several times more, according to industry estimates. Yet operators maintain pricing power because supply physically cannot overshoot demand when power, chips, and construction timelines all act as circuit breakers.

The breakout players

CoreWeave's story validates the entire thesis. The company went public in March 2025 at $40 per share, raising $1.5 billion. Within two months, shares had more than doubled, with the company now trading at a market cap of around $50 billion. The company reported exceptional year-over-year revenue growth in its first earnings release, driven by long-term contracts with Microsoft and OpenAI. The share price has since stabilised after an initial hype cycle.

CoreWeave's success proves that specialised AI infrastructure operators can command software-like valuations despite capital intensity, provided they solve the scarcity equation around GPU access, power, and speed-to-deployment. Similar dynamics are playing out with Nscale in Europe, which raised a record-breaking $1.1 billion Series B to build AI data centres across Europe and other continents.

On the hyperscaler side, the strategies are converging. Microsoft is powering OpenAI's training runs. Amazon's AWS is expanding government-focused AI compute. Google is tuning its TPU roadmap for generative workloads. Meta is building for its LLaMA models, which hit 1 billion downloads in early 2025.

The investment thesis: Infrastructure as the new Alpha

The opportunity isn't just about riding the AI wave. It's about recognising that whoever controls the physical layer controls the value chain. Just as oil infrastructure defined the 20th century, GPU compute capacity and power infrastructure will define the 21st.

For investors evaluating secondary market opportunities or pre-IPO positions, the focus should be on:

Operators with power secured early. First movers with multi-gigawatt grid access will capture disproportionate value as constraints tighten.

Sovereign-aligned projects. Middle Eastern data centre buildouts, European AI sovereignty initiatives, and US national security partnerships offer regulatory moats and patient capital.

Neo-cloud specialists. Companies like CoreWeave that can deliver speed, specialisation, and scarcity premium will command multiples that traditional infrastructure never could.

Enabling infrastructure. Utilities, nuclear partnerships, and renewable energy co-located with data centres represent the picks-and-shovels play.

The underlying technology architecture continues evolving rapidly. For context on how quantum computing and other emerging compute paradigms may reshape infrastructure demand longer-term, the strategic calculus remains similar: control over scarce resources wins.

Bubble or boom?

Critics point to the dot-com parallels: massive capital expenditure, uncertain returns, speculative valuations. But the comparison falls apart on inspection. In 2000, fibre could be overbuilt quickly, creating supply gluts that crashed prices. Today, structural bottlenecks in power, chips, and construction timelines prevent oversupply. Revenue visibility is strong, with hyperscalers signing 3-5 year contracts backed by balance sheets worth trillions.

More importantly, the use cases are real. A majority of companies report positive ROI from AI investments in 2025, according to industry research. This isn't speculative demand; it's enterprises deploying at scale and paying premium rates for reliable compute access.

That said, risks are genuine. Geographic clusters facing power exhaustion could see local corrections. Projects with mismatched debt duration and technology refresh cycles face fragility. Customer concentration, particularly for smaller operators dependent on one or two anchor tenants, remains a vulnerability.

What lies ahead in 2026

The data infrastructure buildout isn't slowing; it's accelerating. Hyperscaler total capex is projected to exceed $600 billion in 2026, a 36% increase over 2025, with the majority flowing into AI-specific capacity. OpenAI's Stargate continues expanding, with sites now operational or under construction in Texas, New Mexico, Ohio, and Michigan. Sovereign funds continue hunting for strategic stakes, viewing compute infrastructure as essential to economic sovereignty in an AI-defined era.

For investors positioned early in high-quality infrastructure assets, whether through specialised cloud operators, data centre REITs, equipment manufacturers, or xAI-style frontier AI plays with captive infrastructure, the opportunity is clear: own the layer that makes intelligence possible.

The gold rush is real. The easy claims are staked. The winners will be those who solve the power equation, secure sovereign partnerships, and build with the flexibility to adapt as AI workloads shift from training to inference. This is the decade when infrastructure became the alpha, and the smart money is moving accordingly.

This article has been prepared using data and analysis from S&P Global, OpenAI, Gulfnews and other sources as cited.

Published by Samuel Hieber