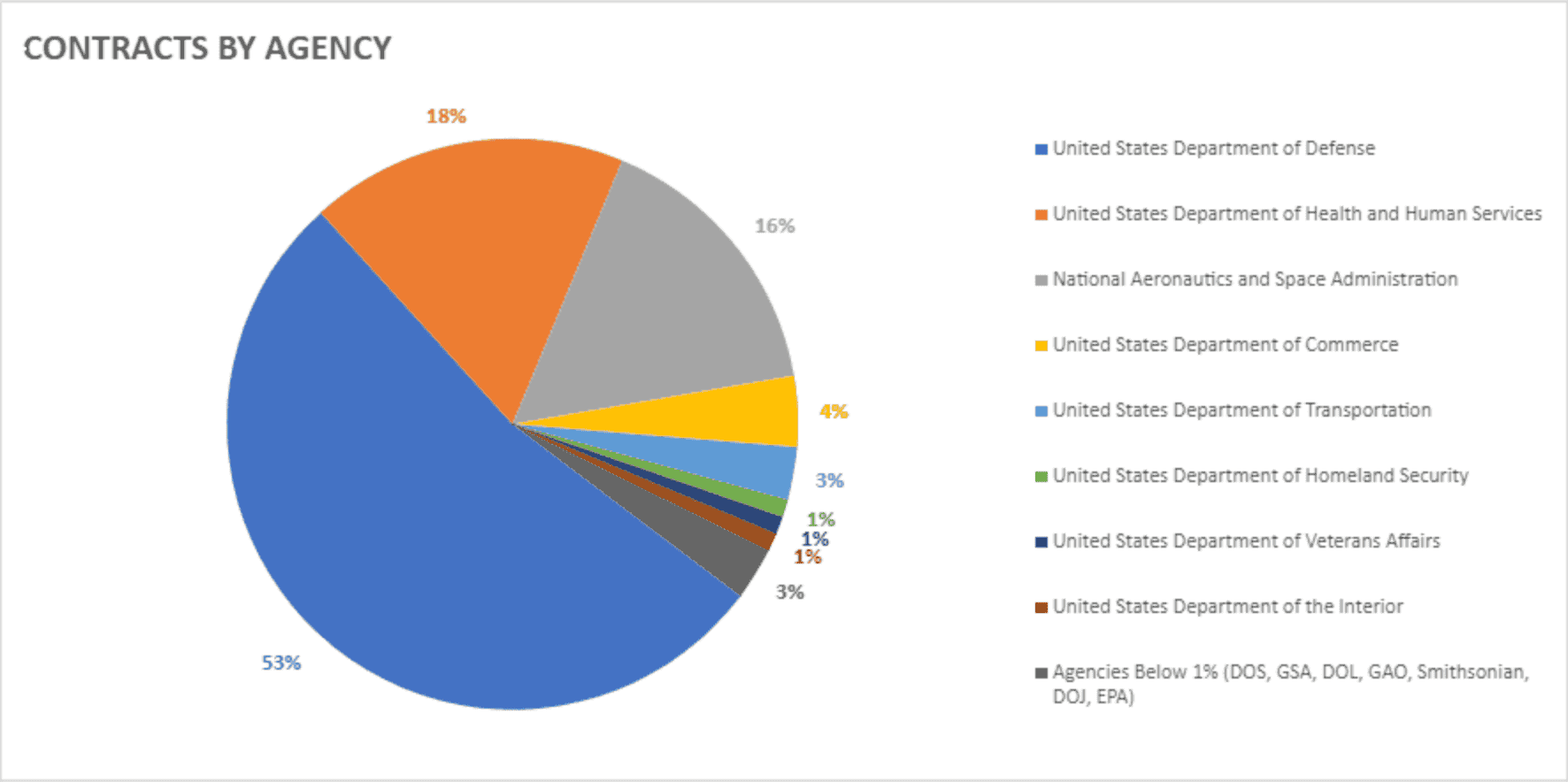

The world’s most powerful AI companies have become instruments of national strategy. Private players like OpenAI, Anthropic, Anduril, and xAI are now embedded inside government systems, securing multi‑billion‑dollar contracts and shaping how states project power. Let's explore their latest endeavors.

The Pentagon’s AI core

In mid‑2025, the U.S. Department of Defense awarded $200 million contracts each to OpenAI, Anthropic, Google, and xAI under an initiative led by its Chief Digital and Artificial Intelligence Office[1]. These deals allow frontier AI models—ChatGPT, Claude, Gemini, and Grok—to run across military and enterprise systems, accelerating adoption of what the Pentagon calls “agentic AI” for mission decision‑making.

OpenAI’s “For Government” program launched weeks earlier, is already testing secure LLMs on defense data prototypes. In parallel, the General Services Administration (GSA) struck “$1 per agency” access agreements, embedding ChatGPT Enterprise across federal agencies[2].

Anthropic mirrored this with “Claude Gov,” trained for classified environments and procured under the same $200 million ceiling. It also signed its own GSA OneGov deal, integrating Claude across multiple departments with FedRAMP‑certified systems[3].

xAI also launched “Grok for Government,” providing AI infrastructure to federal agencies at $0.42 per agency under a GSA partnership directly endorsed by the White House[4].

Together, these contracts turn private AI players into the government’s de‑facto computational infrastructure; outsourcing strategic capacity.

Anduril, Scale AI, and C3.ai: The new defense stack

Anduril became the Pentagon’s most aggressive hardware partner, securing:

- $642 million Marine Corps anti‑drone systems contract

- $22 billion takeover of Microsoft’s Army AR headset program

- $100 million to build next‑gen command‑and‑control frameworks

Scale AI now manages classified data workflows under:

- $100 million OTA contract with the Pentagon

- $99 million Army R&D agreement.

- Thunderforge, a joint AI pipeline integrating models from OpenAI, Anduril, and Microsoft.

C3.ai extended its U.S. Air Force predictive maintenance contract to $450 million[5], now one of the largest production AI deployments in Department of Defense history.

Global expansion and strategic framework

The transformation of AI government capabilities by these players highlights a fundamental truth: tomorrow's geopolitical power will depend less on algorithms than on those who control the physical and regulatory infrastructure underlying AI. The development of this infrastructure is not uniform. It is evolving in distinct regional blocs, shaped by politics, capital, and strategic ambitions.

Region | Key Features & Players | Investment & Capacity Data | Strategic Angle |

|---|---|---|---|

North America | Microsoft, Amazon, Google, Meta lead hyperscale AI infrastructure buildout; OpenAI Stargate initiative | $315-320B AI infrastructure spend in 2025; >40M H100-equivalent chips | Private industry deeply integrated with U.S. state strategy; dominant compute superpower |

Europe | EU AI Act regulates risk; €200B+ for AI Gigafactories and AI Factories; EuroHPC network powers HPC systems | €200B investment mobilized; 20 Gigafactories, 19 AI Factories; data centers consuming up to 40% grid power in hotspots like Amsterdam | Regulation-driven localization; drives sovereignty via hardware and compliance; focus on renewable energy grids and microgrids |

Middle East & Gulf | UAE MGX Fund ($30B), Saudi PIF ($10B+) partner with Google Cloud and Nvidia for sovereign compute hubs | $150B+ committed since 2024; AI-ready data centers with U.S. chip supply chains | Sovereign liquidity buys neutrality; positions region as compute corridor between East and West |

Asia-Pacific | Japan Compute Alliance, India AI Sovereignty Mission drive national compute autonomy | India targets 1M GPUs by 2027; Japan to add 25 exascale sites | Emerging regional compute independence; reducing U.S. cloud dependency |

Our 6 investment takeaways

The contracts and initiatives detailed above are not isolated events. We see them as signs of a fundamental shift in how technological value is created and captured. From an investment standpoint, this new realm demands a new framework. We base our strategy on six takeaways:

1. We follow strategy, not sentiment. Capital now aligns with state priorities, not market momentum. Defense, AI, and infrastructure deals increasingly mirror geopolitical intent rather than consumer trends.

2. We measure strategic dependency, not user metrics. The real value lies in how irreplaceable a company is to a government. Firms like Anthropic or Anduril succeed because they are embedded in national security architectures, not because of scale alone.

3. We view regulation as an economic moat. Regulatory frameworks—export controls, classified model governance, FedRAMP approvals—are becoming the new pricing power. Companies built within these layers capture durable, compliant demand.

4. We treat AI defense as critical infrastructure. These businesses now function like regulated utilities: predictable cashflows, strong political backing, and sovereign-linked revenue streams across compute, data, and sensor infrastructure.

5. We position for asymmetric consolidation. A handful of “AI primes” will dominate the ecosystem, while smaller innovators become acquisition targets. Our focus remains upstream—where value compounds in compute, security, and interoperability.

6. We redefine liquidity and exit expectations. As long-term government contracts tighten market float, we anticipate alternative exit paths—structured buybacks, sovereign partnerships, and perpetual capital vehicles.

[1] https://www.nextgov.com/acquisition/2025/07/pentagon-awards-multiple-companies-200m-contracts-ai-tools/406698/

[2] https://www.nextgov.com/acquisition/2025/08/openai-give-federal-agencies-chatgpt-access-1-year/407266/

[3] https://www.gsa.gov/about-us/newsroom/news-releases/gsa-strikes-onegov-deal-with-anthropic-08122025

[4] https://www.gsa.gov/about-us/newsroom/news-releases/gsa-xai-partner-to-accelerate-federal-ai-adoption-09252025

[5] https://investorsobserver.com/news/stock-update/largest-ai-deployment-in-u-s-defense-c3-ai-ai-stock-lands-350m-pentagon-deal/

Published by Samuel Hieber